What Every Buyer Should Know

Saving up to buy a home can feel a little intimidating, especially in today’s market. For many first-time buyers, the idea that you have to put 20% down can feel like a major hurdle.

But here’s the good news: that’s actually one of the biggest myths in real estate.

Do You Really Need To Put 20% Down?

Unless your specific loan type or lender requires it, chances are you won’t need to put down 20%. In fact, there are loan programs designed specifically to help first-time buyers get into a home with a much smaller down payment.

For example:

FHA loans allow down payments as low as 3.5%

VA and USDA loans often require no down payment at all for qualified buyers

While putting more down can reduce your monthly payments or eliminate mortgage insurance, it's not a must. As The Mortgage Reports puts it:

“. . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . . the 20 percent down rule is really a myth.”

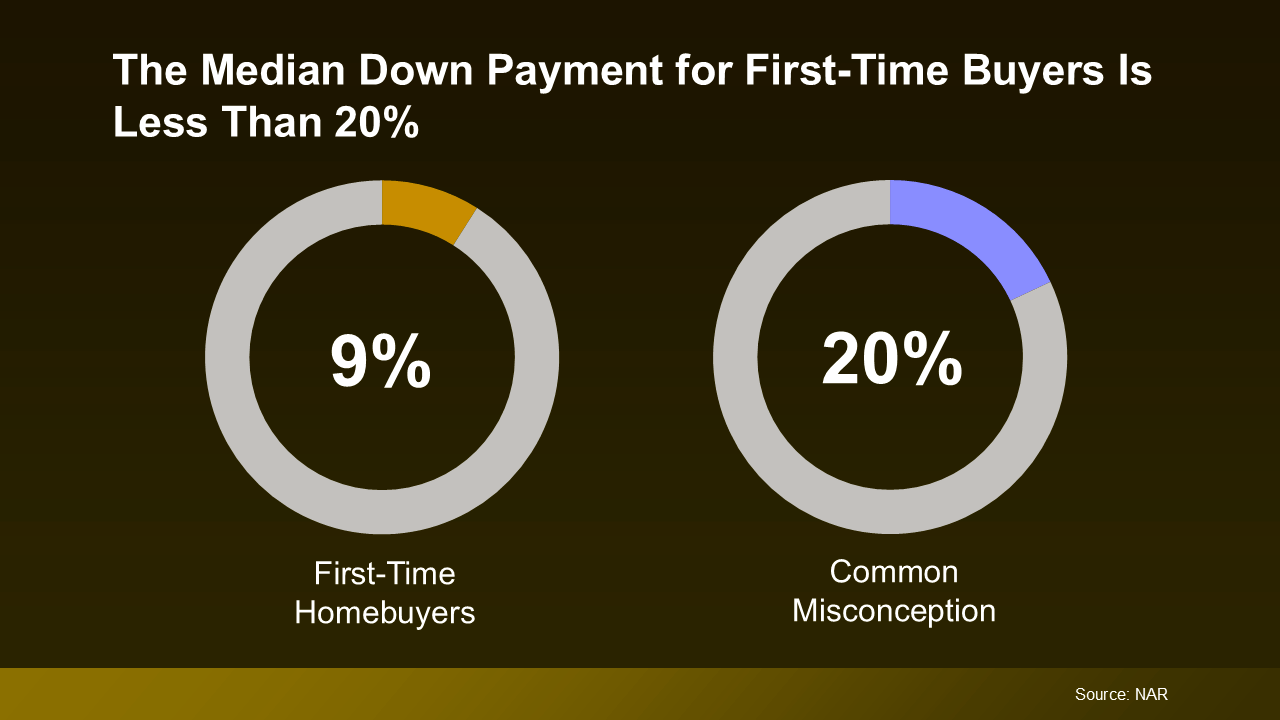

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is just 9%—a far cry from 20%.

Down Payment Assistance Could Be a Game-Changer

Here’s another surprising stat: nearly 80% of first-time homebuyers qualify for down payment assistance (DPA), yet only 13% actually use it. That means many buyers are leaving thousands of dollars on the table. Some of these programs offer an average of $17,000 toward your down payment or closing costs. “Our data shows the average DPA benefit is roughly $17,000. That can be a nice jump-start for saving for a down payment and other costs of homeownership.” – Rob Chrane, Founder and CEO of Down Payment Resource. In some cases, buyers can even stack multiple programs together, giving your savings an even bigger boost.

Why Talking to a Trusted Lender Matters

At The Glover Team, we believe the financing side of buying a home shouldn’t be stressful. That’s why we encourage you to connect with one of our trusted lenders to get a personalized look at your loan options, including down payment assistance and lower-down-payment programs. We work well with all lenders, and you're always welcome to choose the one that feels right for you. That said, working with our preferred lending partners often leads to a more seamless experience, with better communication, faster responses, and smoother closings for everyone involved.

Our Preferred Lenders

Ron Ricchio

Chicagoland Home Mortgage Services

773-557-1000

Archie E Vetter

Neighborhood Loans

708-261-5583

Bottom Line

You don’t need to wait until you’ve saved 20% to buy a home. Many buyers put down far less, and there are programs available that could make homeownership even more accessible.

Let’s chat about your options. Whether you’re just starting to plan or ready to buy, The Glover Team is here to guide you, and connect you with the right professionals every step of the way.